Mark Robyn, a senior associate at The Pew Charitable Trusts, researches and analyzes fiscal federalism.

States are waiting for Congress to act on an income tax provision that affects many of their residents – the deduction for state and local sales taxes. This federal deduction expired at the end of 2014, and if it is not extended, people in states with no or limited income tax would be most affected. In recent years, policymakers have approved one- or two-year extensions of the sales tax deduction as part of a broad package of temporary tax laws known as the “tax extenders.” But as of now the deduction is expired and will not be available for people to claim on their 2015 tax returns unless Congress passes the tax extenders bill.

What is the state and local sales tax deduction?

Tax filers who itemize deductions on their federal returns may deduct certain taxes paid to state and local governments, such as real estate, personal property, and income taxes. Under this provision, filers could choose to deduct state and local sales taxes instead of income taxes, but that option expired at the end of 2014. About 10 million filers claimed a total of $17 billion in state and local sales tax deductions in 2013, the most recent year for which data is available.

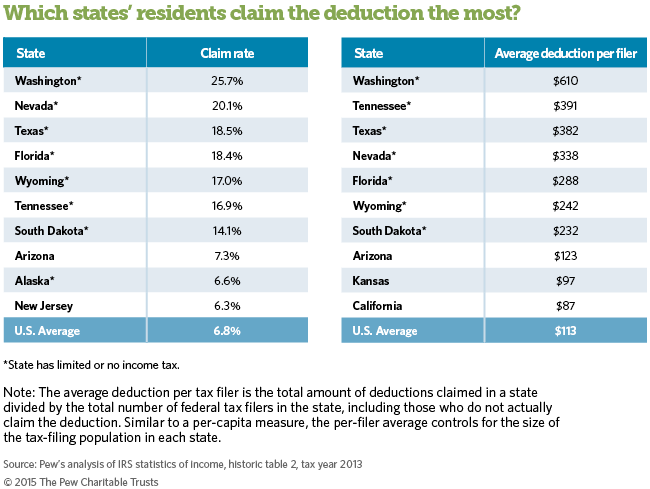

Nationwide, about 7 percent of all filers claimed the sales tax deduction in 2013 and the average deduction per tax filer was $113. However, because filers must choose between deducting income or sales taxes, the claim rate and average amount were significantly higher in eight states with no or limited income tax. In Washington state, for example, which has a sales tax and no income tax, nearly 26 percent of federal filers claimed the deduction in 2013 and the average deduction per filer was $610 (see table showing the top 10 states). States that have income taxes tend to have lower claim rates because many filers deduct income instead of sales taxes.

How do the deductions for state and local taxes affect states?

Federal deductions for state and local taxes—including real estate, personal property, and income or sales taxes—lower the taxes paid by individuals who claim them and so reduce the overall cost to taxpayers of state and local spending. Effectively, the federal government covers a share of the cost of state and local services. The Congressional Budget Office and the Congressional Research Service have suggested that state and local governments may be more likely to impose higher taxes that are deductible at the federal level and to provide more services because of this deduction. Changes to these deductions, such as the expiration of the sales tax deduction, could affect states’ decisions about their own tax policies, including the level and mix of taxes. If these deductions were reduced or eliminated, states with the highest claim rates and average per-filer deductions would be most affected.

Heavily armed officers stand by a security checkpoint at Hartsfield-Jackson Atlanta International Airport after terrorist attacks in Paris. Experts say that smaller U.S. cities may lack the resources needed to prevent or react to an attack. AP

For Tuscaloosa, Alabama, there are lessons to be learned from the terror that gripped Paris just over a week ago.

After the Islamic State attacks, Democratic Mayor Walter Maddox took note of the Parisian security staff that prevented a suicide bomber from entering the French national soccer stadium. His thoughts turned to Bryant-Denny Stadium—where more than 100,000 people gather for University of Alabama football games.

Maddox said he considered what could happen in his 95,000-person city. But he and some terrorism and security specialists say many chief executives and police departments in midsize U.S. cities may not realize that terrorism could put their people and infrastructure at just as much risk as high-profile targets like New York City and Washington, D.C.

“The larger cities understand and grasp this,” Maddox said. “I’m not sure that at the midlevel cities the awareness is that high.”

But terrorism can and does happen in those places. This year, two men suspected of communicating with overseas terrorists were killed when they attempted to attack a free-speech event in Texas, a gunman killed four people at a military recruiting center in Tennessee, though it was unclear if he had worked with known terrorist organizations, and security was heightenedacross the country during Fourth of July weekend.

In the days following the Paris attacks New York City deployed the first 100 officers in the city’s new Critical Response Command. The 500-officer program will be dedicated to counterterrorism in the city, which spent $170 million this year to bring 1,300 new police officers to its 34,500-officer force.

Conversely, in Wichita, Kansas, where an airport worker was arrested after he tried to execute a suicide attack at the local airport in 2013, the 437-officer police force was struggling to stay fully staffed this summer.

While it’s difficult to tell just how prepared every state and municipality is for a potential terrorist attack, security specialists say the ability to prevent and react well depends on a communication system and local counterterrorism efforts that are still underdeveloped, even 14 years after 9/11.

Chet Lunner, a security consultant and former senior official at the U.S. Department of Homeland Security (DHS), said the FBI has counterterrorism investigations in every state, but most places probably lack the resources to prevent or respond to an attack.

“You might think that all 50 states are responding to that kind of warning, but I’m not sure that they are at the appropriate level,” Lunner said.

The Paris attacks on “soft” targets like the restaurant and the concert hall—places with minimal security—should signal to local governments in the U.S. that they, too, could be at risk.

Lunner and Michael Balboni, a security consultant and former New York state senator who wrote homeland security laws for his state, say even if smaller cities and towns aren’t at high risk for violence and are short on the financial resources that big cities have, they should still plan and practice for terrorist attacks.

“State and local personnel are literally the tip of the spear,” Lunner said. “They owe it to themselves as well as the communities they serve” to be as prepared as possible.

Communication Is Key

Despite repeated efforts and hundreds of millions of dollars spent on collecting and sharing information nationwide about potential terrorist threats, questions remain about how much filters down to local officials, especially in smaller municipalities.

In 2003, DHS and the U.S. Department of Justice began creating fusion centers to encourage and ease the sharing of information between federal law-enforcement and counterterrorism officials in states and major urban areas. But a 2012 U.S. Senate subcommittee report found the centers yielded little counterterrorism intelligence.

In 2011, the White House released the first national strategy and plan to empower local governments to prevent domestic violent extremism and homegrown terrorism. The plan advocates enhancing federal engagement with local communities that may be breeding grounds or targets for violence, though it has been criticized for disproportionately focusing on and alienating Muslims.

Until there is centralized information-sharing between the national and local governments, it will be difficult to get localities invested in sustained antiterrorism work, Balboni said.

Balboni, who also served as a New York state homeland security adviser, said the fusion centers need to morph into what he calls “command and control centers” that gather intelligence and work in places where a potential threat or terrorist activity surfaces.

Outside Big Cities

People who don’t live in big cities typically viewed as likely terrorist targets may not think about terrorism affecting their communities or about devoting the resources to countering the possibility they could be hit. But they ought to.

Less-populated locales are where terrorists may settle in to plan or practice attacks, Lunner said. It is up to local police to get to know people and seek out information about potential threats.

“In this country, if you dial 911, the CIA does not show up at the end of your driveway,” Lunner said.

In Minot, a North Dakota city of less than 50,000, dealing with terrorist threats became a reality in the wake of the Paris attacks as the names of six people stationed at the Minot Air Force Baseappeared on an Islamic State hit list.

The biggest challenge in responding to such a threat, Police Chief Jason Olson said, is the limited amount of resources his department has to focus on gathering intelligence and analyzing data.

Minot is a good example of a place that many would not typically consider to be at risk for terrorism. And all Olson and local officials can do is push for relevant and timely information from the federal government. But, Lunner said, they are probably not as informed as their counterparts in places like New York City.

Although states were quick to spend billions of federal dollars funneled to them after 9/11, they couldn’t sustain salaries needed to run long-term local surveillance programs with that one-time infusion of money. Since then, local spending on antiterrorism has been reduced, said Doug Farquhar, a program director with the National Conference of State Legislatures.

“The problem is that they knew this was one-time dollars,” Farquhar said. “You can buy a firetruck or build a building, but you can’t hire employees.”

Localities have also been unlikely to pay more attention to antiterrorism because of the infrequency of attacks, he said.

Maddox said Tuscaloosa is unique in its willingness to dedicate money and resources to prepare for terrorism and disaster. He credits much of that willingness to training that he and his staff received from the Federal Emergency Management Agency, in 2009.

“It’s getting your team to believe that we need to prepare for a moment that may or may not ever come,” he said.

Disaster Prep Equals Terror Prep

For many states and municipalities, counterterrorism has become just a part of general disaster preparation, Farquhar said.

Maddox, who has been credited with an exemplary response to a 2011 tornado that destroyed 12 percent of the city, said the same elements of responding to a natural disaster or a major violent crime—providing emergency medical care, shelter and food, and good law-enforcement—extend to counterterrorism.

“Whether we have a natural disaster or an active shooter situation, my protocols are going to be nearly identical in how we approach that situation,” he said.

And in Minot, which has suffered a number of disasters in recent years—including a train derailment and subsequent ammonia spill, a chemical warehouse fire and historic flooding—Olson said responding to terrorism has become just a part of the disaster preparedness plan.

Security team members at the Mall of America near Minneapolis train in February following a terrorist threat. Dozens of bills were filed across the country this year to beef up training of security guards and tighten industry oversight, but most went nowhere. (Getty Images)

At an Iowa mall, a security guard allegedly shot and killed a woman who worked at a children’s museum there. At a Kentucky distillery, a security guard accepted money from thieves to look the other way while they stole more than $100,000 in expensive whiskey. And in a Virginia hospital, a 64-year-old man suffered a serious head injury and later died after a violent altercation with a security guard.

Recent incidents like these have drawn fresh attention to the screening, training and state oversight of private security officers, and have prompted some legislators to push for stricter regulation—efforts that have been largely unsuccessful this year.

“We’ve got to feel comfortable that people who have a badge on are, in fact, trained—and trained well,” said Michigan state Sen. Darwin Booher, a Republican who sponsored a set of bills, still pending, that would update regulations on security guards in the state.

About 90 bills were introduced in state legislatures this year dealing with the licensing and training of security officers or requirements for security companies, according to Steve Amitay, director of the National Association of Security Companies (NASCO), an industry group. In recent years, similar numbers of measures have been proposed. None of this year’s bills that would have substantially toughened state requirements was enacted, Amitay said.

“In some of these states, it’s a very anti-regulatory environment and they think any additional regulation on businesses or people performing services is bad,” Amitay said. “With other folks, it’s a resource issue. For the state to start regulating an industry and requiring licenses requires initial appropriations and startup costs.”

In Connecticut, a bill that would have required security guards to get more training died in the Senate. In Washington state, a measure that would have mandated FBI criminal background checks for all applicants never made it to the House floor.

In California, Democratic Gov. Jerry Brown vetoed a bill that would have made bouncers and plainclothes guards subject to the same licensing requirements that apply to private security officers.

Forty-one states, plus the District of Columbia, license security officers, but requirements vary greatly from state to state. Alaska, for example, mandates 48 hours of training initially, plus another eight hours in firearms training for armed guards. South Carolina requires four hours of training and an additional four for those who carry a gun.

While nine states—Colorado, Idaho, Kansas, Kentucky, Mississippi, Missouri, Nebraska, South Dakota and Wyoming—do not license security officers at the state level, some cities within them do, according to NASCO. Mississippi does require that guards get a separate permit to carry a gun. And 22 states have no training requirements for unarmed security guards; 15 of those have none for armed guards, either.

“It’s a hodgepodge. It’s an extreme variety of approaches,” said Charles Nemeth, a professor at John Jay College of Criminal Justice who directs its Center for Private Security and Safety. “Some are better than others; some are nonexistent.”

Training Varies

More than 1 million security guards work in retail stores, hospitals, sports stadiums and other locations, according to the U.S. Bureau of Labor Statistics. They typically are responsible for protecting property, enforcing rules, conducting security checks and deterring criminal activity, and had a median salary of $23,970 in 2012.

Most work for a security company that contracts its services. Others are hired directly by a business or corporation.

While the vast majority don’t carry weapons, those that do have raised special concerns. A 2014investigation by the Center for Investigative Reporting and CNN found poor oversight and little accountability of the armed guard industry. Twenty-seven states did not check whether armed guard applicants were in a federal database banning them from carrying a gun and nine did not conduct federal criminal background checks, the investigation revealed.

There are no federal standards for training security officers—armed or unarmed—so it’s left to the states. Basic training usually involves learning how to administer CPR, the proper use of force, how to deal with the public and fill out reports, and how to report suspicious activities and interact with police.

Sandi Davies, director of the International Foundation for Protection Officers, a nonprofit that gives training certificates to security guards, said states should require at least 40 hours of basic training—most don’t.

“We want a more trained and skilled officer to protect our premises. They need to be able to identify threats,” Davies said. “I can’t for the life of me think that anyone should be in a position of authority without at least 40 hours of training.”

Amitay of NASCO said his group, which represents many of the larger security companies, also supports higher standards and training requirements, and many of its members’ background checks and training go beyond what states require.

The thousands of smaller security companies that operate may or may not do the same. “In some states,” Amitay said, “all you need is a business license and you can start a private security firm and hire people off the street.”

Some small security companies have fended off legislative attempts to beef up regulations, Amitay said. Additional requirements could be costly for them because they would have to outsource training or hire trainers, he said.

But opposition doesn’t only come from smaller companies, Davies said. “Sometimes, the large contract agencies don’t want to spend the money because it really affects their bottom line. They have the lobby power.”

Legislative Efforts

Some legislators who support stricter regulation of the private security industry say they are disappointed their efforts this year haven’t succeeded.

Connecticut Democratic state Rep. Stephen Dargan, who co-chairs the Joint Public Safety and Security Committee, said the spate of school shootings and other mass shootings in recent years has increased the sense of urgency.

“With what’s going on around the country right now and after our horrific incident in Newtown, we thought this was an important issue,” Dargan said. The committee introduced and passed the security guard legislation, which died in the Senate. It would have hiked the required training hours for licensed guards from eight to 16 and mandated 16 hours of firearms training for armed guards.

“Sometimes, you get pushback from some of these security companies,” Dargan said. “Often, in tough economic times, it’s the cost factor.”

In Michigan, which currently does not require training, a set of bills is still in play that would update regulations and require 32 hours of training for security guards and another four for those armed with guns.

Booher, who sponsored the package, said he has tried to get this type of legislation passed for several years, but faced opposition from some colleagues who balked at adding, rather than eliminating, regulations. The measures cleared the Senate this spring and have been referred to a House committee.

“It’s been slow going. But then we had a person killed at a mall near Detroit by a security guard last year, so more and more legislators have become interested,” Booher said. “It’s been a long time coming.”

Job Risks

Security officers’ jobs can be dangerous and sometimes their efforts can be heroic.

In 2009, a guard died in a shootout with a white supremacist at the United States Holocaust Memorial Museum in D.C. Last year, a drugstore guard in Detroit was killed trying to save a woman and child from a carjacking in the store’s parking lot. And in Pennsylvania, a 70-year-old high school security officer was stabbed in the chest while trying to stop an attack by a teenager who allegedly stabbed 20 of his classmates. The guard and the injured students survived, and the suspect was arrested.

A 2012 Bureau of Labor Statistics study found that security guards were fatally injured in the workplace at a rate more than twice that of workers in general.

The threat of terrorism in recent years also has brought greater attention to the role of security guards, particularly at malls and other “soft targets.”

While the industry is trying to prepare for these threats, John Jay’s Nemeth said, it still faces a more basic problem: It is not thoroughly screening entry-level officers before hiring them.

“I think the largest problem security faces is bad people,” Nemeth said. “There’s been a tremendous de-emphasis on whether you have good character or not, like whether you’ve been arrested in the past for drug use or you can’t get good references from people who know you.”

When security officers get into trouble, it often involves sexual misconduct or internal theft and fraud, Nemeth said. “There are many more cases of that than of security guards shooting people. Stealing is a massive problem in the retail sector.”

Davies, of the training foundation, said the industry also needs to hike salaries and reduce turnover. Ultimately, her group would like to see a national standard of 60 to 80 hours of training.

“Your security officer is often your first responder,” Davies said. “With today’s threats—workplace violence issues, school shootings—you want this person to be prepared and well trained. Bringing someone in with little or no training, what’s the value? It’s more of a detriment, and it can be the difference between life and death.”

Vehicles are pulled off on the shoulder during bad traffic congestion, on Interstate 495 outside of Washington. Maryland and D.C. have issued regulations to prevent individual consumer data from being used to set insurance rates. AP

When Fred and Donna Wolden’s biannual car insurance premium went up by $90 last month, they wanted to know why.

The Wisconsin retirees hadn’t had an accident or bought a new vehicle. In fact, they say not much has changed in the two-plus decades they’ve insured their home and cars through AAA. The couple is used to premium increases of 5 to 8 percent, but this year’s 20 percent increase has them wondering if it is the result of “price optimization,” a rate-setting method rooted in consumer spending habits that is drawing the scrutiny of state insurance regulators around the country.

Ten states (California, Florida, Indiana, Maine, Maryland, Ohio, Pennsylvania, Rhode Island, Vermont and Washington) and the District of Columbia have warned insurance agencies not to use individual spending habits or a history of shopping around to predict how big a price increase a customer will tolerate.

The Woldens’ renewal notice shows that AAA used a consumer report to help determine their premium, but they say they haven’t been able to obtain a copy of the report.

Critics of the practice say that when insurers drill down to individual consumer data, such as purchase records from credit cards or supermarket club cards, they can end up charging different rates to customers who pose the same insurance risk. But the insurance industry says it analyzes consumer data to rate groups of customers, not individuals, and that the practice helps them offer fair and stable pricing.

In Rhode Island, the most recent state to warn against price optimization, the move was pre-emptive, said Paula Pallozzi, who works for the Rhode Island insurance division. There is no evidence that insurance companies are using the technique.

Douglas Heller, a consultant for the Consumer Federation of America (CFA), said he thinks that insurance companies are evaluating individual policyholders on factors unrelated to risk and that state regulators want to get in front of technology that provides access to consumer data.

“There’s a reasonable concern that if they let the horse out of the barn, that insurance companies will get so technologically out ahead that insurance regulators will really lose their ability to oversee the industry,” he said.

The restrictions on price optimization vary in each state, but regulators generally have limited insurance companies’ ability to use consumer information that is unrelated to a policyholder’s level of risk. The Rhode Island bulletin specifies that insurers must base rates, and the classes in which they lump customers, on factors related to expected losses and expenses.

The Woldens said a AAA representative couldn’t explain the premium hike when they called about it, but the insurer did knock $21 off their premium—after inquiring about the couple’s former occupations and education levels. The Woldens acknowledge their ages (they are both over 70) may have contributed to the rate change, but say their “insurance scores”—measures of their finances and credit—have not changed significantly.

After reading about price optimization—and other rate-setting practices—the Woldens speculated that the tactic could be linked to their rate increase. AAA said it does not publicly discuss the details of individual policies.

“We just think there’s something here that they’re using that we can’t put our finger on,” Fred Wolden said.

Newly Available Data

Because electronic transactions make consumers’ purchasing history readily available, consumer advocates say insurers are looking beyond typical risk factors, like driving records and credit scores, to “optimize” rates.

In doing so, insurance companies sometimes work with third-party vendors to develop a customer analysis based on a range of data, said Heller, the CFA consultant. That could include information, he said, about whether a customer has shopped around for insurance, where she regularly shops or what kind of products she buys.

“I suspect nobody is revealing [their rating factors] because it’s entirely inappropriate and it would creep people out,” Heller said.

But Robert Hartwig, an economist and the president of the Insurance Information Institute, a nonprofit backed by the insurance industry, said insurance companies use consumers’ data to analyze groups, not individuals. Hartwig said the abundance of consumer data helps insurance companies set accurate, competitive prices, which lead to a stable marketplace.

“As insurers collect more information, just like any industry, they are able to perform sophisticated analyses,” he said. “It creates a set of rates that’s more accurate than any time in history.”

Regulations on price optimization ultimately won’t affect how insurance companies do business, Hartwig said, because insurers don’t use data to evaluate individual customers, but instead evaluate the risk associated with groups of policyholders.

Competitive Markets

Judging market conditions before setting rates is a natural move for the insurance industry. And, as in other industries, insurance companies have to be able to set prices based on market data to stay competitive, Hartwig said.

“It is a competitive marketplace and it is quite reasonable for an insurer to try to determine what impact a new product might have on profit,” Hartwig said, noting that insurance markets lack the volatility of markets for airline tickets or food.

But Heller and other consumer advocates say factors used in price optimization are not indicative of risk, and such pricing hurts low-income drivers and homeowners, who may be less likely to shop around because they are not financially savvy.

“With price optimization, they argue that it gives them tools to judge the market better,” Heller said. “But this isn’t an equivalent of selling flowers or a plane ticket. It’s something the government mandates every driver purchase.”

The insurance market is more favorable to low-income purchasers than many other markets: it does not include penalties for switching to better or cheaper products. Furthermore, Hartwig said, the price of insurance policies does not go up and down based on the time of purchase the way airfare prices do.

He also rejects the idea that low-income customers might not shop around for better insurance rates. He points to an Insurance Institute survey that indicated 68 percent of respondents making less than $35,000 a year compared insurance prices at various agencies by phone, on the Internet or in person.

State legislation requires Arizona Gov. Doug Ducey to request tougher Medicaid eligibility requirements every year from federal overseers. (Creative Commons photo by Gage Skidmore)

If Arizona gets its way, its able-bodied, low-income adults will face the toughest requirements in the country to receive health care coverage through Medicaid.

Most of the those Medicaid recipients and new applicants would have to have a job, be looking for one or be in job training to qualify for the joint federal-state program for the poor. They would have to contribute their own money to health savings accounts, which they could tap into only if they met work requirements or engaged in certain types of healthy behavior, such as completing wellness physical exams or participating in smoking cessation classes. And most recipients would be limited to just five years of coverage as adults.

Despite its conservative bent, Arizona already has expanded Medicaid under the Affordable Care Act. In October, however, Republican Gov. Doug Ducey will ask the federal agency that oversees Medicaid to approve changes in the state’s program that are designed to promote healthy behavior in a traditionally unhealthy population, while encouraging people to become less economically dependent on the state.

“The governor wants to help them move from a place of dependence on the state to independence and to be able to take care of their own health needs,” said Christina Corieri, the governor’s health care adviser. The proposals would not apply to several categories of beneficiaries, including children, pregnant women, the disabled and the elderly.

Some of Arizona’s proposals have been made in other states, and the federal government has signed off on them. It has rejected work requirements, however, and has never allowed lifetime limits on eligibility.

The work requirement and lifetime limit originated in legislation passed by the Arizona Legislature earlier this year. The law requires the governor to submit the same proposals every year, apparently in the hope that a future Republican presidential administration would look at them more favorably.

Critics say denying health care to people who don’t meet the new standards punishes them for being poor.

“I think in some of (the proposals), we see a punitive strain and an assumption that, left to themselves, people will make bad choices and that we the government will make better choices for them,” said Joan Alker, executive director of the Center for Children and Families at Georgetown University.

The Center on Budget and Policy Priorities, a nonpartisan research organization in Washington, D.C., notes that 60 percent of Medicaid recipients live in a family with at least one full- or part-time worker.

Health Savings Accounts

Though Arizona passed its Medicaid expansion in 2013, more recently a number of states have used expansion as an opportunity to gain greater flexibility from the federal Centers for Medicare and Medicaid Services, or CMS, in how they administer the program.

For example, CMS has allowed Arkansas, Indiana and Michigan to require or encourage beneficiaries to contribute to tax-advantaged HSAs. Beneficiaries can use the accounts toward copays—the portion of their medical bills not paid by Medicaid—or for health-related services not covered by Medicaid, such as dental, vision or chiropractic care. The idea is to force enrollees to build their own safety net to help cover their health care costs.

In Arizona, beneficiaries would have to contribute up to 2 percent of their annual household income to their HSAs.

But only beneficiaries who meet Arizona’s work requirements or health behavior goals—such as completing well-patient visits or adhering to regimens for patients with chronic conditions—would be permitted to access their HSAs. And beneficiaries earning above the poverty level—$11,770 for an individual—who failed to make their HSA contributions could be suspended from Medicaid benefits for a period of six months; those earning less than the poverty level would be deemed to owe the state a debt.

Other states have received permission to impose similar penalties. For example, Indiana charges a premium to all Medicaid recipients and can cancel the enrollment of those making more than the poverty level for six months if they fail to make their premium payments. The poorest Indiana beneficiaries do not owe a debt to the state if they don’t pay their premiums, but they lose eligibility for enhanced medical services, such as vision or dental care.

Arkansas imposes a debt on the poorest beneficiaries who do not make payments into their HSAs and it can deny Medicaid services to those making above the poverty level for failure to do so.

Arizona, which has 1.7 million Medicaid beneficiaries, also isn’t the first state to try to encourage beneficiaries to adopt healthy behaviors. Several states—such as Indiana, Iowa, Michigan, Minnesota and New York—include what are called healthy behavior incentives in their Medicaid programs, to nudge people to lose weight or stop using tobacco.

In Iowa, for instance, participants are asked to have a wellness examination once a year. People who meet their health targets in Indiana, Iowa and Michigan will see their premiums or HSA payments reduced or eliminated altogether.

Minnesota gives cash or debit cards to beneficiaries with pre-diabetes who participate in a YMCA diabetes prevention program. In New York, beneficiaries can receive cash or lottery tickets for keeping doctor’s appointments or filling prescriptions for nicotine replacement therapy or drugs to manage high blood pressure or diabetes.

If approved by CMS, Arizona’s Medicaid plan would be the first to use deterrents, rather than incentives, to push healthy habits. Those who don’t meet established goals could be shut out from access to their HSAs. (They’d also forgo the chance to reduce their mandatory HSA contributions in the future.)

Working for Coverage

Arizona is asking permission for two provisions that CMS has not granted to any other state: establishing employment requirements and imposing a lifetime limit on Medicaid coverage.

Indiana proposed a work requirement, but it was shot down by CMS in January. The agency said that while states may promote employment through state programs operated outside of Medicaid, they could not do so under the Medicaid program.

Instead of being able to impose work requirements, Indiana and New Hampshire have had to settle for referring Medicaid applicants to jobs and job training as a requirement for receiving coverage.

Several health advocacy organizations in Arizona object to policies to exclude otherwise eligible people from Medicaid, which they say are contrary to the program’s intent.

“We see some of these proposals as inconsistent with the Medicaid law, which is to have a safety-net program to provide access to health care to a population that doesn’t otherwise have that,” said Tara McCollum Plese, a senior director with the Arizona Alliance for Community Health Centers. “To take these people out of Medicaid at a time they still need health care services is not prudent.”

Some national groups, such as Families USA, agree.

“Medicaid is designed to be an affordable option for people and putting a time limit on it is poor public policy in keeping people covered and healthy,” said Dee Mahan, Medicaid director for Families USA, which advocates for affordable health care. “Lots of people are working at low-wage jobs, and at low-wage jobs on a part-time basis, and their incomes are not necessarily going to increase to the point where they can get out of Medicaid.”

Others question the effectiveness of some restrictions. The Urban Institute, a nonpartisan policy research organization, found that HSAs have high administrative costs. It also said that wellness programs have not been shown to be effective.

On the other side, Americans for Prosperity, the conservative advocacy organization co-founded by billionaires Charles and David Koch, strongly favors the Arizona proposals, particularly the work requirement.

“It reduces dependency on government and encourages able-bodied folks to work,” said Boaz Witbeck, the organization’s Arizona policy analyst.

After Arizona submits its proposals to CMS, there will be a monthslong review process, during which there will be room for negotiation between the state and the federal agency.

When then Gov. Jan Brewer, a Republican, won approval for Medicaid expansion in 2013, Arizona’s plan did not include these provisions. The current governor is not threatening to pull back from expanded Medicaid coverage if the federal government rebuffs the state’s proposals, according to Dan Scarpinato, his communications deputy.

“The focus right now is on getting approval on this waiver, and we are hopeful,” Scarpinato said.

In 2014, Aileen Rizo, depicted here with her parents, Paul and Lupe Rizo, sued her employer for wage discrimination after she says she found out her male colleagues were paid much more. States are addressing the wage gap between men and women.In 2014, Aileen Rizo, depicted here with her parents, Paul and Lupe Rizo, sued her employer for wage discrimination after she says she found out her male colleagues were paid much more. States are addressing the wage gap between men and women. AP

Aileen Rizo says she loves what she does. A consultant for the Fresno County Office of Education in California, she teaches educators how to teach math. She’s got the experience, 20 years, and the education, two master’s degrees.

But over a casual lunch three years ago, her colleagues shared their salaries. Rizo, 41, the only full-time woman in her office, was startled to discover that some of her male co-workers—including a new hire with less experience and education—were being paid at least $10,000 more than she was. When she confronted her employer, she was told her salary was based on her prior wages. End of story. No negotiating. Rizo sued the county, and her case is pending in U.S. District Court.

While too late to be of any aid to Rizo, the California Legislature this month sent Democratic Gov. Jerry Brown a “pay equity” bill designed to help women in situations like hers. The bill—which some call the strongest of its kind in the nation and Brown has indicated he will sign—attacks the gender wage gap in several ways, including ensuring women who perform similar work receive the same pay as men, even if their job titles are different.

And California isn’t alone in acting. In the absence of legislation from the U.S. Congress, the governors of Connecticut, Delaware, Illinois, North Dakota and Oregon have signed equal pay laws this year. New York legislators unanimously passed a bill that Democratic Gov. Andrew Cuomo has indicated he will sign. And Massachusetts has two bills pending.

Equal pay bills also were introduced in 21 other states, but didn’t pass, according to the American Association of University Women (AAUW), which has lobbied for the legislation.

“If Congress can’t legislate its way out of a paper bag, we’ll go to the state legislatures and the city councils,” said Lisa Maatz, vice president of government affairs for the AAUW. “State legislators are paying attention.”

But some critics, such as Daniel Mitchell of the Cato Institute, a libertarian think tank in Washington, said that the new legislation would put a “catastrophic burden” on businesses.

“The notion that there’s some widespread discrimination in the marketplace, there’s just no real-world evidence for it,” Mitchell said. “They’re trying to give the government widespread authority to make very abstract judgments about the value of a job in the private sector.”

The move to outlaw disparate pay arrives as new studies indicate that American women earn 79 percent of what men earn doing comparable work. Using white men’s earnings as a baseline, the wage gap is even worse for African-American women, who earn 63 percent of what white men earn. Latinas earn 54 percent of what white men earn. Faring better than other minority women, Asian-American women earn 90 percent of what white men earn.

In California, women earn 84 cents for every dollar men earn, according to the National Women’s Law Center (NWLC), an advocacy group based in Washington. It is 83 cents in Connecticut, 81 cents in Delaware, 71 cents in North Dakota and 82 cents in Oregon. Louisiana has the biggest gap, with women making 65 cents for every dollar that men make; the District of Columbia has the smallest, with women making 90 cents for every dollar that men do.

State legislation is important because it provides protections for workers and closes loopholes that employers have used to circumvent state and federal laws, said Fatima Goss Graves, a senior vice president at the NWLC.

Nationally, two bills—the Paycheck Fairness Act, which would penalize employers who retaliate against employees for discussing their salaries with their co-workers, and the Fair Pay Act, which would require equal pay for comparable work—are stalled in Congress.

“States are doing what they can to give workers new tools to address the wage gap,” Goss Graves said, adding that some states, such as California, are providing greater protections than the would-be federal laws.

“This can have a spillover effect,” Goss Graves said. “The wage gap hasn’t changed in a lot of years. Employers pay women less in the same job as men and the laws aren’t strong enough to be a deterrent. This is an issue people want a solution to. They don’t want to wait another 50 years for the wage gap to close.”

While the laws overwhelmingly draw bipartisan support in the statehouses, the California bill faced some pushback for not being inclusive enough. The California chapter of the National Organization for Women opposed it because it didn’t protect lesbian, gay, bisexual and transgender people or men of color, who also face wage discrimination.

A Persistent Problem

The pay gap has barely budged in a decade. In 2014, women working full time were paid 79 cents for every dollar men were paid—a 2-point increase from 2004. At that rate, AAUW estimates, women’s pay won’t catch up to men’s for another 100 years.

Nor does education close the gap. In nearly every occupation, women face pay disparities, according to the Institute for Women’s Policy Research (IWPR), a Washington think tank. If anything, professions requiring college degrees see even greater gaps, said Ariane Hegewisch, study director for the IWPR.

The reasons for the gap are complex. Women sometimes are not as effective as men in negotiating their salaries, women’s advocates and legal analysts say. The “motherhood penalty,” a term for the disadvantages facing working mothers relative to childless women, plays a part. Outright discrimination is often a factor.

Sometimes, however, discrimination by employers is inadvertent. Unconscious bias on the part of employers can create inequitable wage practices, according to Beverly Neufeld, founder of PowherNY, a statewide network for economic equality which advocated for the New York pay gap bill.

“There’s no doubt that equal pay for equal work is the law of the land,” Neufeld said. “The question is, ‘What gets in the way of that law and what is the reality for women in the workforce?’ ”

As was possibly the case with Rizo, Neufeld said that women often start out, right out of school, making less than their male counterparts. Because most jobs offer pay based on previous salaries, they never catch up. And if employers prohibit workers from disclosing their salaries to their colleagues, some analysts say, they’ll never know that they’re being underpaid in the first place.

Due to occupational segregation, women tend to cluster in “pink ghetto” jobs, further contributing to the inequity, according to IWPR’s Hegewisch.

For example, in the female-dominated library sciences field, you typically need a master’s degree to even snare an interview. But in the male-dominated engineering field, a bachelor’s degree is usually all that’s needed to find work. And engineers earn much more than librarians, Hegewisch said.

“Women aren’t getting paid equally for the same job,” said Maatz of the AAUW. “But there’s also this devaluation of what is considered women’s work.”

California Remedies

California was the first state to pass a pay gap law—in 1949, more than a decade before John F. Kennedy signed the federal Equal Pay Act, in 1963. The laws were largely identical, with similar flaws and weaknesses, said Jennifer Reisch, legal director for Equal Rights Advocates, a San Francisco-based national organization that helped draft the 2015 California bill.

Neither law was strong enough to enforce, according to state Sen. Hannah-Beth Jackson, a Democrat from Santa Barbara and the sponsor of the bill in California. Women in California are drastically underpaid, Jackson said, leading to an estimated $33.6 billion in lost wages every year.

“My hope is that this bill will encourage employers to take a close and careful look at their pay practices to ensure that women are being paid equally for substantially similar work, so that complaints and lawsuits can be prevented,” Jackson said.

Her bill, which applies to the private and public sector, would close loopholes that prevent enforcement of existing pay discrimination laws. It would allow employees to discuss salaries with other employees without fear of retaliation from employers. (California legislators also passed a related bill that would prevent employers from asking potential hires about their previous salary history.)

“We hope that this law will be a model for other states and perhaps even for the federal efforts,” Reisch said.

It would ensure that women who perform similar work to men receive the same pay, even if their job titles are different or they work in different offices. Under federal law, employees seeking to make a wage discrimination claim against an employer can only compare their wages to someone in the same workplace.

The California bill also has a “comparable worth” provision, which means that you can’t pay one employee a different rate if you have employees of a different gender doing substantially similar work.

The bill would encourage employers to rank jobs objectively by skill, effort, responsibility and working conditions, Maatz said. So, say you have a parole officer and a child services social worker. Parole officers tend to be overwhelmingly male, while social workers tend to be female. Both jobs require a similar amount of education; both jobs are fairly dangerous. But parole officers are paid much more, Maatz said.

“Hopefully this will motivate businesses to do the right thing from the get-go,” Maatz said. “We want a law that’s strong enough that business will behave proactively.”

Some states and municipalities have tried different ways to tackle the gender wage gap.

In Vermont, for instance, employers are required to print salary descriptions in job advertisements to prevent a potential hire from being haunted by a previous low salary. For the past 30 years, Minnesota has had a “comparable worth” law on the books for state workers. And earlier this year, Democratic Mayor Kasim Reed of Atlanta signed an equal paylaw for municipal employees that would require the city to identify pay disparities and find remedies for them.

Rizo said she felt strongly enough about California’s new pay equity bill that she testified and lobbied for it.

But the Fresno County Office of Education said Rizo wasn’t discriminated against.

“I am certain that there has never been any disparity in pay based on gender because men and women are placed on the salary schedule using the same criteria,” said Jim Yovino, the Fresno County superintendent. “We are confident that the case has no merit and have requested the court to dismiss the lawsuit.”

Rizo says that with her lawsuit pending, work is a tense place to be. But quitting her job is out of the question. She’s the mother of three, and her husband is a full-time student. They depend on her income, she said. And as the mother of three daughters, she felt like she needed to fight for equal pay to set an example for them. Quitting would send the wrong message.

Passing the law, Rizo said, “assures me that my fight has not been in vain. I feel victorious no matter what happens with my case.”